How I Smartly Funded My Kid’s Sports Training — And Protected Every Dollar

Paying for your child’s sports training can feel like a financial leap in the dark. You want them to thrive, but costs add up fast — equipment, travel, coaching, and more. I’ve been there, juggling expenses while worrying about returns. What if the investment doesn’t pay off? This is the full story of how I approached youth sports funding like a real financial decision — balancing passion, planning, and protection — so you don’t have to guess what works.

The Rising Cost of Youth Sports: A Family Finance Challenge

Youth sports have evolved far beyond casual weekend games in the park. What once required only a pair of cleats and a uniform now often demands year-round training, private coaching, travel tournaments, and high-end equipment. For many families, supporting a child in competitive athletics has become one of the most significant recurring expenses, rivaling even private school tuition or summer camps. According to national surveys, the average family spends between $500 and $2,000 annually per child on sports-related costs, with elite programs pushing that figure well over $5,000 in some cases. These numbers aren’t limited to high-profile sports like hockey or gymnastics — even baseball, soccer, and swimming can carry substantial price tags when pursued at a competitive level.

What makes this financial burden particularly challenging is its unpredictability. Unlike fixed monthly bills, sports expenses fluctuate based on the season, competition schedule, and unexpected needs such as last-minute travel or injury rehabilitation. A single out-of-state tournament can cost hundreds in registration, transportation, lodging, and meals. Equipment replacement — whether it’s a new bat, cleats, or a specialized training device — adds up quickly, especially as children grow and outgrow gear. Medical co-pays from sports injuries, though often overlooked, can also strain household budgets. These costs don’t just affect disposable income; they can jeopardize longer-term financial goals like saving for college or retirement if not managed strategically.

Yet many families approach youth sports spending reactively, treating it as an emotional necessity rather than a planned financial commitment. The desire to support a child’s dreams can override budgeting instincts, leading to overspending and financial stress. This emotional component is understandable — no parent wants to hold their child back. But without clear boundaries and planning, even well-intentioned support can lead to long-term consequences. Recognizing that youth sports are no longer a low-cost extracurricular but a major family expense is the first step toward responsible financial management. When families acknowledge the true cost, they can begin to make informed decisions rather than impulsive ones.

Moreover, the financial impact is not evenly distributed. Middle- and lower-income households often face difficult trade-offs, choosing between sports participation and other essentials. Some children may be excluded from competitive programs simply because their families cannot afford the associated costs. This economic barrier can limit access to valuable experiences that build confidence, teamwork, and discipline. Addressing these disparities begins with transparency about costs and a commitment to planning. By treating youth sports funding as a serious financial matter, families can ensure that participation remains sustainable and equitable, without sacrificing other critical financial priorities.

Beyond Passion: Viewing Sports Training as a Financial Commitment

Passion is the engine that drives children to wake up early for practice, push through fatigue, and strive for improvement. But passion alone cannot pay the bills. Smart families understand that supporting athletic development requires more than emotional investment — it demands a structured financial approach. When parents begin to view sports training as a financial commitment, similar in weight to education or healthcare, they shift from reactive spending to proactive planning. This mindset change is crucial. It allows families to evaluate not just the immediate costs, but the long-term implications of their choices, ensuring that enthusiasm does not override financial responsibility.

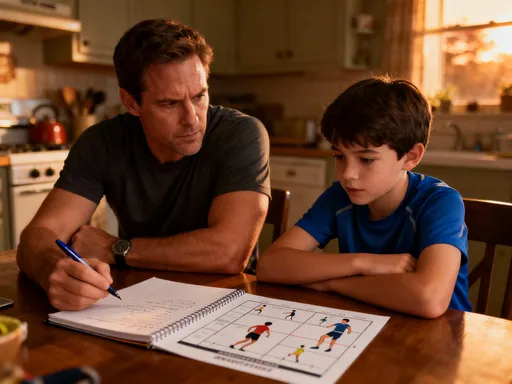

A key distinction lies between recreational and competitive sports. Recreational programs are typically seasonal, community-based, and low-cost, focusing on participation and fun. Competitive sports, on the other hand, often involve year-round training, private coaching, travel teams, and higher entry fees. The financial jump between these two paths can be dramatic. A child moving from a local soccer league to a travel team may see costs increase three- or fourfold. Recognizing this shift is essential. Families must ask themselves: Is this a long-term path, or a short-term goal? How committed is the child? What are the realistic outcomes? These questions help align financial decisions with actual expectations, reducing the risk of overspending on an uncertain future.

Assessing a child’s level of commitment is not always straightforward. Enthusiasm at age ten does not guarantee dedication at fifteen. Parents should engage in regular, honest conversations with their children about their goals, enjoyment, and willingness to put in the effort. These discussions should include financial transparency — helping children understand that resources are limited and choices must be made. Involving kids in budget conversations fosters responsibility and appreciation, teaching them that opportunities come with trade-offs. For example, a family might decide that attending a national tournament means postponing a family vacation. When children understand this balance, they are more likely to value the experience and remain committed.

Additionally, families should consider the developmental trajectory of their child’s sport. Some sports, like swimming or gymnastics, require early specialization and intensive training to reach elite levels, while others, such as baseball or basketball, allow for later skill development. Understanding these timelines helps families plan more effectively. Early investment may be justified in sports where peak performance occurs in the late teens, but less so in sports where college recruitment begins later. Researching typical pathways — such as when scouts start attending games or when college programs begin outreach — can inform smarter financial decisions. The goal is not to discourage participation, but to ensure that spending matches realistic opportunities and long-term goals.

Building a Safety Net: Risk Management for Sports-Related Spending

Every financial decision involves risk, and youth sports are no exception. The risk isn’t just financial — it includes injury, burnout, changing interests, and program cancellations. A well-structured financial plan accounts for these uncertainties by incorporating safeguards that protect the family’s overall stability. Without such protections, a single setback — like a season-ending injury or a canceled tournament — can derail not only athletic aspirations but also household finances. Risk management in youth sports funding is not about limiting potential; it’s about ensuring that support remains sustainable, even when things don’t go as planned.

One of the most effective tools is the emergency fund. Families should establish a dedicated reserve for sports-related emergencies, separate from general household savings. This fund can cover unexpected medical expenses, last-minute travel changes, or equipment damage. Even a modest buffer of $1,000 can prevent the need to dip into retirement accounts or accumulate credit card debt. The key is consistency — contributing a small, regular amount over time rather than scrambling when a crisis arises. Automating transfers to this fund makes it easier to maintain without constant oversight.

Spending caps are another critical component. Before each season, families should set a maximum budget for sports-related expenses and stick to it. This includes not only direct costs like registration and coaching but also indirect ones like meals on the road, laundry, and time off work. Once the cap is reached, no additional funds are allocated, regardless of opportunities or peer pressure. This discipline prevents emotional overspending and ensures that other financial goals remain intact. It also teaches children about boundaries and priorities, reinforcing that resources are finite.

Contingency planning is equally important. Families should discuss what happens if a child gets injured, loses interest, or decides to pursue a different path. Will unused funds be saved for future use, redirected to another activity, or returned to the general household budget? Having these conversations in advance reduces stress during difficult moments. Additionally, some families explore insurance options that cover sports injuries or program interruptions. While not always necessary, these policies can provide peace of mind, especially for high-risk sports or expensive international competitions. The goal is not to eliminate risk — that’s impossible — but to manage it wisely, so that passion and prudence coexist.

Smart Funding Strategies: Balancing Savings, Income, and External Support

Funding youth sports doesn’t have to mean sacrificing other financial goals. With thoughtful planning, families can support athletic development without draining savings or accumulating debt. The key is to adopt a multi-pronged approach that combines disciplined saving, strategic income generation, and external support. This balanced strategy ensures that sports funding is sustainable, predictable, and aligned with the family’s overall financial health.

One of the most effective methods is establishing a dedicated savings account specifically for sports expenses. This account should be separate from general household funds to avoid accidental overspending. Families can set up automatic monthly transfers, even if the amount is small — $50 or $100 per month adds up significantly over a year. Treating sports funding like a recurring bill reinforces its importance and ensures consistent progress. Some parents tie contributions to family milestones, such as adding a bonus deposit after a tax refund or birthday gift. This approach builds a financial cushion gradually, reducing the pressure of large, one-time payments.

Performance-linked incentives can also motivate both financial responsibility and athletic effort. For example, a family might agree to cover tournament fees if the child maintains a certain grade point average or completes a set number of volunteer hours. This creates a sense of accountability and teaches the value of earning opportunities. Similarly, some families offer to match funds that children save themselves — whether from allowance, part-time jobs, or holiday gifts. This not only reduces the parental burden but also instills financial literacy and personal investment in the sport.

External support is another valuable resource. Community sponsorships, though more common in rural or tight-knit areas, can provide meaningful assistance. Local businesses may be willing to sponsor a young athlete in exchange for recognition at events or on social media. Fundraising efforts — such as car washes, bake sales, or crowdfunding campaigns — can also generate additional income while building community engagement. These initiatives teach children about teamwork, communication, and initiative, extending the benefits beyond the field.

Finally, families should review their existing budgets for potential reallocations. Sometimes, small adjustments in other areas — such as reducing dining out, switching to more affordable entertainment options, or canceling unused subscriptions — can free up hundreds of dollars annually. These savings can then be redirected toward sports funding without impacting essential needs. The goal is not austerity, but intentionality — making conscious choices that reflect family priorities. When savings, income, and external support work together, the financial burden becomes manageable, and the focus can remain on growth and development.

Measuring Value: What “Return” Really Means in Youth Sports

When discussing financial investment, many people instinctively think of monetary returns — scholarships, professional contracts, or future earnings. While these outcomes are possible, they are statistically rare. Less than 1% of high school athletes receive full college athletic scholarships, and even fewer go on to play professionally. Relying on financial payback as the sole measure of success sets families up for disappointment. A more meaningful approach is to redefine “return” in terms of personal growth, life skills, and long-term opportunity.

Youth sports offer invaluable benefits that extend far beyond the scoreboard. They teach discipline, resilience, time management, and teamwork — qualities that serve children well in academics, careers, and relationships. The ability to handle pressure, work toward long-term goals, and collaborate with others are skills that cannot be easily quantified but are essential for lifelong success. These intangible returns often outweigh any financial gain, shaping character and confidence in ways that last a lifetime.

Families can track progress through non-financial milestones. Improved performance, leadership roles on the team, sportsmanship awards, or personal bests are all valid indicators of growth. Regular check-ins — quarterly or seasonally — allow parents and children to reflect on what has been learned, what challenges have been overcome, and whether the experience remains fulfilling. This ongoing evaluation helps ensure that participation continues to align with the child’s interests and development.

At the same time, families must remain open to reassessment. There may come a point when the financial cost no longer matches the personal benefit. A child may lose interest, face persistent injuries, or realize that their passion lies elsewhere. Recognizing these moments is not a failure — it’s a sign of wisdom. Continuing to invest heavily in a path that no longer serves the child can lead to resentment, burnout, and financial strain. Knowing when to step back, redirect, or transition to a less intensive level is a crucial part of responsible financial stewardship. The true return on investment is not a trophy or a scholarship, but a happy, healthy, well-rounded child.

Avoiding Common Financial Traps in Competitive Youth Sports

Even the most well-meaning families can fall into financial traps when supporting youth sports. These pitfalls are often driven by emotion, social pressure, or misleading marketing rather than sound financial judgment. Recognizing these patterns early can prevent costly mistakes and preserve both financial stability and family harmony.

One of the most common traps is overspending on elite programs with unproven results. Some training academies and travel teams promise exposure to college scouts or professional pathways, yet deliver inconsistent outcomes. Families may pay thousands for access to networks that never materialize. Before enrolling in any high-cost program, parents should research its track record, talk to other families, and evaluate whether the benefits justify the expense. If a program guarantees results or uses high-pressure sales tactics, it’s a red flag.

Peer pressure is another powerful influence. Seeing other families invest heavily can create a sense of urgency or inadequacy. But just because a neighbor pays for private coaching doesn’t mean it’s necessary or effective. Each child’s path is unique, and comparisons can lead to unnecessary spending. Staying focused on personal goals, rather than external benchmarks, helps maintain financial discipline.

Emotional decision-making is perhaps the hardest trap to avoid. The desire to give a child every opportunity can cloud judgment, leading to impulsive purchases or last-minute registrations. Implementing a cooling-off period — waiting 48 hours before making any significant sports-related purchase — can help families make more rational choices. It allows time to consult with partners, review budgets, and consider alternatives.

Finally, ignoring long-term consequences can be dangerous. Diverting funds from retirement, college savings, or emergency reserves may seem manageable in the short term, but it creates future risk. Sustainable support means protecting the family’s financial foundation while investing in the child’s present. By recognizing these traps and adopting a thoughtful, evidence-based approach, families can avoid common pitfalls and make choices that benefit everyone in the long run.

Planning Ahead: Integrating Sports Costs into Long-Term Family Finance

Supporting a child in sports is not a one-season decision — it’s a long-term commitment that requires ongoing planning. Sustainable funding means looking beyond the next tournament and integrating sports expenses into the broader family financial picture. This includes aligning sports budgets with education savings, healthcare planning, and retirement goals. When all financial priorities are considered together, families can make balanced decisions that support both current passions and future security.

Open communication between spouses is essential. Both partners should be involved in financial discussions, sharing responsibilities and agreeing on spending limits. Disagreements about sports funding can create tension, especially if one parent feels the burden more heavily. Regular financial check-ins — quarterly or semi-annually — help ensure alignment and allow for adjustments as circumstances change. Involving children in age-appropriate conversations also builds financial awareness and responsibility.

Flexibility is key. A child’s interests, skill level, and goals will evolve over time, and financial plans should adapt accordingly. A shift from competitive to recreational play, a change in sport, or a decision to focus on academics should all be met with supportive, not punitive, financial responses. The goal is not to lock in a rigid path, but to create a framework that allows for growth, change, and balance.

In the end, responsible funding isn’t about cutting back — it’s about building a stronger foundation. When passion and prudence grow together, families can support their children’s dreams without compromising their financial well-being. By planning wisely, protecting resources, and measuring success beyond money, parents can give their children the greatest gift of all: the freedom to pursue their potential, safely and sustainably.